Loanable Funds Market

Loanable funds market

- hypothetical market that illustrates the market outcome of the demand for funds generated by borrowers and the supply of funds provided by lenders

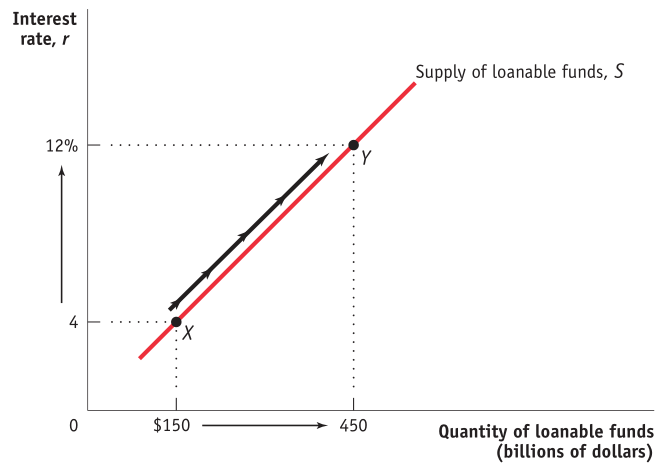

Savers are the ones who save the money and thus are more willing to lend out at higher rates of return

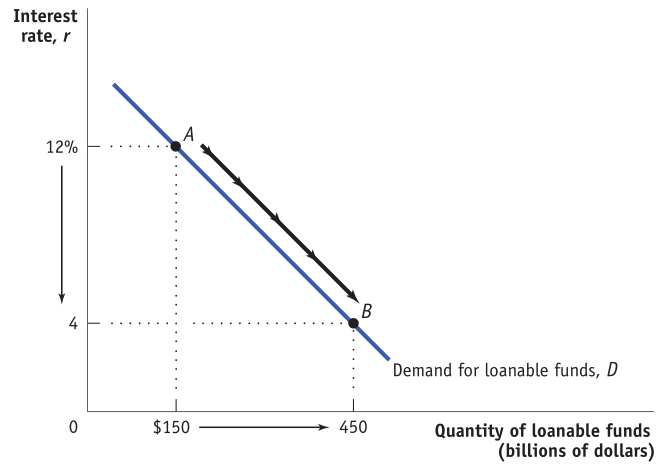

Borrowers (ie. firms with investment spending projects) prefer lower interest rates

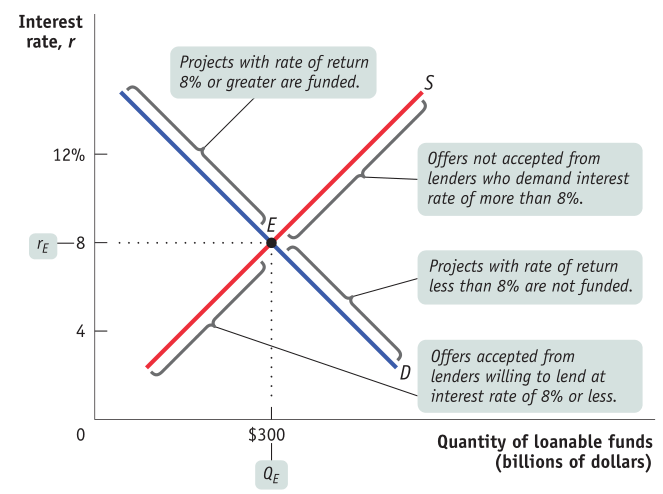

Equilibrium in the Loanable Funds Market

- quantity of funds that savers want to lend equals the quantity of funds that businesses want to borrow

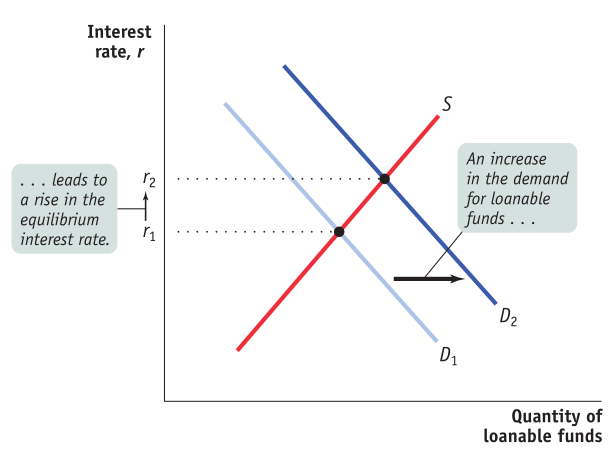

Shift of Demand for Loanable Funds

Changes in perceived business opportunities

If businesses see opportunities of higher return, the demand for loanable funds will increase

In the late 1990s with the dot com boom, firms were excited about any possible internet company out there and the demand for loanable funds increased to right

Changes in the government's borrowing

When governments incur a deficit, the demand for loanable funds will increase

Crowding out occurs when interest rates increase and therefore, businesses will invest less. Thus, the crowding out effect

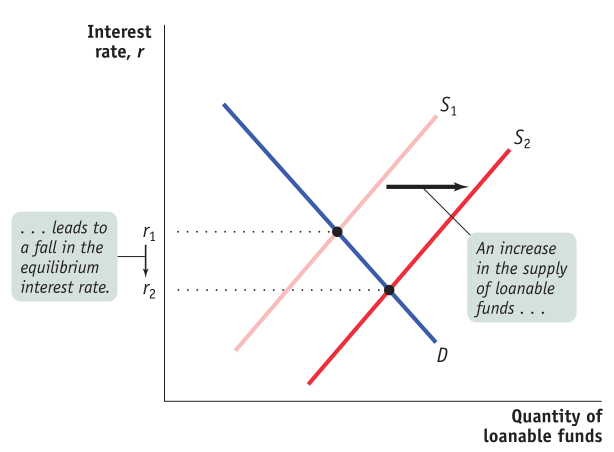

Shift of Supply for Loanable Funds

Changes in private saving behavior

Between 2000 and 2006, rising home prices caused people to "feel richer" and therefore spend more and save less

The supply of loanable funds, therefore, would shift to the left as a result

Changes in capital inflows

With a large inflow of capital funds, the supply of loanable funds shifts to the right

Conversely, when international investors flee (like in Argentina), the supply of loanable funds shift to the left

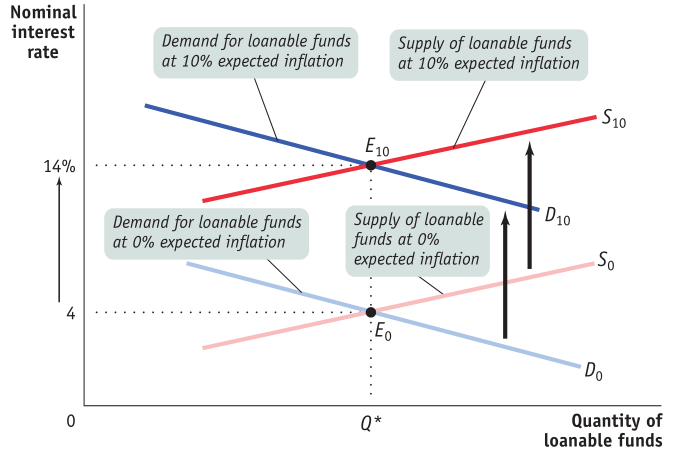

Inflation and Interest Rates

Inflation will tend to help borrowers and hurt savers

In the late 1970s and early 1980s, homeowners "won" with inflation and banks "lost" with inflation

Real interest rate = Nominal interest rate - inflation rate

The true cost of borrowing is the real, not nominal, interest rate!

A good "hedge" against inflation would be to buy a house and take on a low-interest rate mortgage and invest in other assets, perhaps the stock market

Fisher effect

The expected real interest rate is unaffected by the change in expected future inflation.

Borrowers and lenders base decisions on the expected real interest rate not the nominal

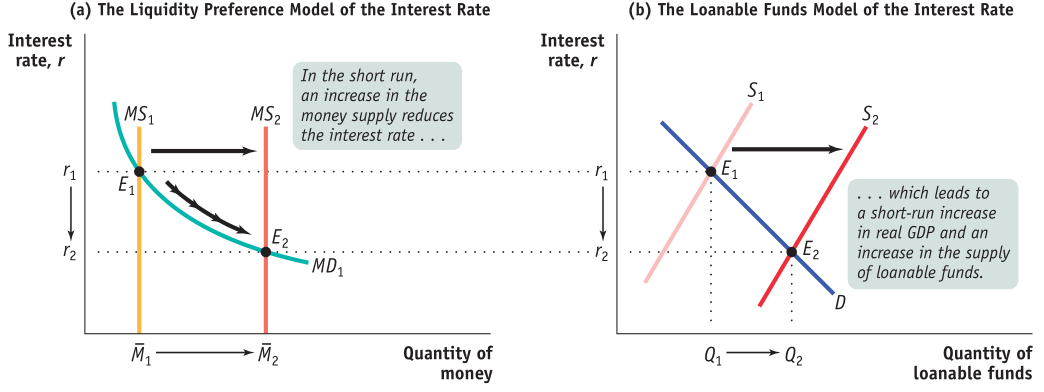

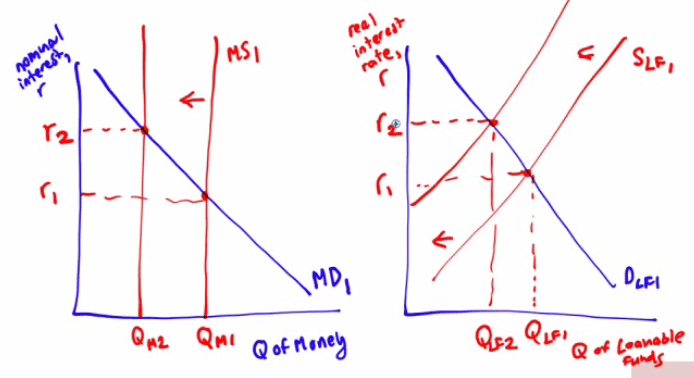

Interest Rate in the Short Run

A fall in the interest rates leads to a rise in investment spending, which leads to a rise in GDP, which leads to a rise in savings

In the money market, an increase in the money market shift the MS to the right, lowering r

In the short run, the loanable funs market follows the lead of the money market.

The change in GDP increase savings(investment) and shifts supply of loanable funds to the right

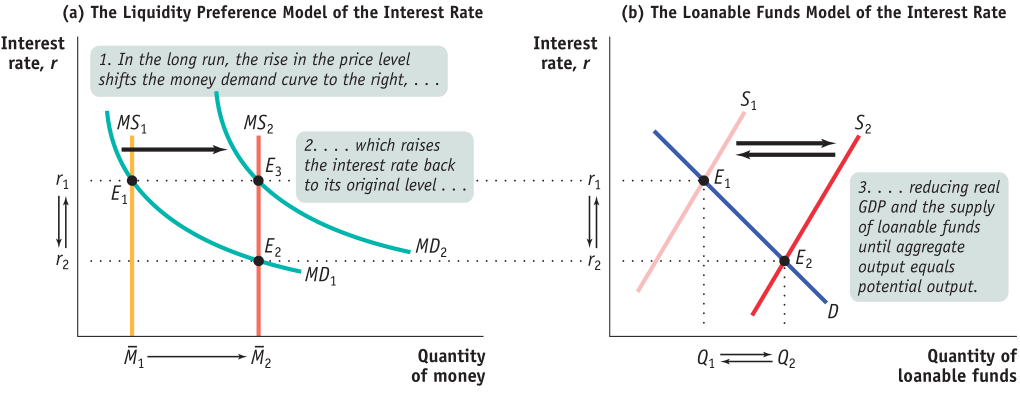

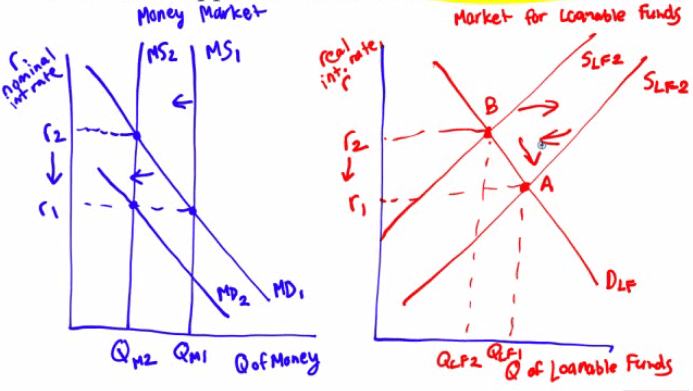

Interest Rate in the Long Run

In the long run, however, when the money supply increases, the aggregate price level increase and therefore the money demand increase in the same proportion

So, MS1 shifts to MS2, but MD1 shifts to MD2, which raises the interest back to its original level

As a result, the supply of loanable funds which originally shifted to the right, shifts back to the left, back to its original level!

In the long run, money doesn't matter!

The supply and demand for loanable funds determines the interest in the long run

Practice Question

If the Fed sells government securities, what happens in the money market? What will happen in the loanable funds market in the short-run?

In the long-run, if the Fed sells government securities, what happens in the money market? What will happen in the loanable funds market?

Does each of the following affect either the supply or demand for loanable funds, and if so, does the affected curve shift to the right or shift to the left

Decreases in capital inflow into the economy

↓ Supply of Loanable Funds, Shift Left

Business are optimistic about future business conditions

↑ Demand for Loanable Funds, Shift Right

The government decreases borrowing

↓ Demand for Loanable Funds, Shift Left

The private savings rate increases

↑ Supply of Loanable Funds, Shift Right